📞 (858) 308-1100

✉️ contact@veslav.com

Understanding Owner’s Compensation in Different Business Structures: Sole Proprietorships, Partnerships, and Corporations

10/31/20243 min read

How you, as a business owner, compensate yourself depends greatly on your business structure. Each structure has unique rules and tax implications for compensation, and misunderstanding these can lead to costly mistakes. This post explores the differences in owner’s compensation across various business types – including sole proprietorships, single-member LLCs, partnerships, S corporations, and C corporations – and offers tips to avoid common errors.

Why Correctly Handling Owner’s Compensation Matters

Misclassifying compensation can lead to penalties, higher taxes, and inaccurate financial records. Properly handling owner’s compensation:

Ensures compliance with tax laws

Accurately reflects owner contributions and business expenses

Prevents personal tax overpayments or underpayments

Let’s examine each structure in detail to understand how you should approach compensation.

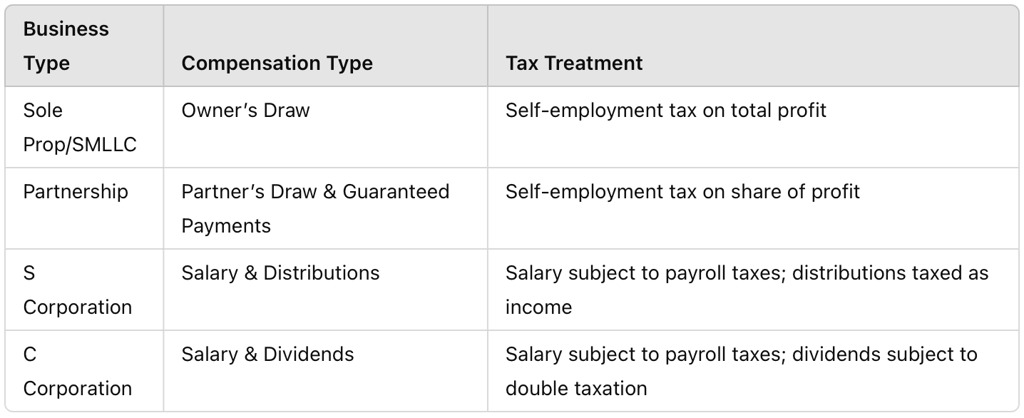

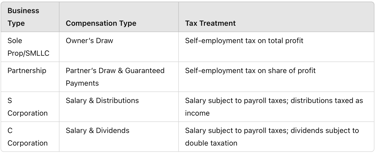

1. Sole Proprietorships & Single-Member LLCs (SMLLCs)

Compensation Method: Owner’s Draw

In a sole proprietorship or SMLLC, there’s no distinction between the owner and the business, so the IRS considers profits as personal income to the owner. Therefore, you don’t receive a salary as you would in a traditional employment scenario. Instead, you take an owner’s draw.

Owner’s Draw: You can withdraw funds from the business account as needed, and these withdrawals are recorded as “Owner’s Equity” or “Owner’s Draw” in QuickBooks.

Taxes: You’re taxed on the total profits of the business, not the draw amount itself. Profits pass through to your personal tax return, where you pay self-employment taxes.

Avoiding Common Mistakes

Avoid Recording Draws as Salary or Wages: Owner’s draws are not expenses and should not be categorized as payroll.

Set Aside Taxes: Since no taxes are withheld, consider setting aside a percentage of each draw to cover quarterly estimated taxes.

2. Partnerships

Compensation Method: Partner’s Draw

In a partnership, profits and losses are shared among partners, typically according to a partnership agreement. Like sole proprietorships, partners don’t receive a traditional salary; instead, they take a partner’s draw.

Partner’s Draw: Partners can withdraw from business profits throughout the year, recorded in QuickBooks as a “Partner Draw” or under “Partner’s Equity.”

Guaranteed Payments: If partners receive guaranteed payments (a form of compensation regardless of profit), these payments are treated as business expenses and are reported on the partners’ K-1 tax forms.

Taxes: Each partner reports their share of business income or losses on their personal tax return, paying self-employment taxes on their total earnings from the partnership.

Avoiding Common Mistakes

Don’t Confuse Draws with Payroll: Draws should not be categorized as payroll expenses.

Handle Guaranteed Payments Correctly: Guaranteed payments must be set up in QuickBooks as expenses to the partnership, not as personal income distributions.

3. S Corporations

Compensation Method: Salary and Distributions

In an S corporation, the IRS requires shareholder-employees who provide services to the business to receive a reasonable salary. This approach satisfies the need for Social Security and Medicare taxes, which are avoided on distributions alone.

Salary: The owner takes a regular salary, with tax withholdings, recorded as payroll. This salary must be reasonable according to IRS guidelines based on industry and role.

Distributions: Profits beyond the salary can be taken as distributions, which are not subject to self-employment taxes.

Taxes: Salaries are subject to regular payroll taxes, while distributions are only taxed as income on the owner’s personal tax return.

Avoiding Common Mistakes

Set a Reasonable Salary: Failure to take a reasonable salary or only taking distributions can trigger IRS audits and penalties.

Keep Salary and Distributions Separate: Record each separately in QuickBooks – salary as payroll expenses and distributions as shareholder distributions or equity.

4. C Corporations

Compensation Method: Salary and Dividends

C corporations are unique in that they are separate tax entities. Shareholder-employees can receive salaries and dividends from the business.

Salary: The owner receives a salary like any other employee, with standard withholdings for taxes.

Dividends: Profits distributed to shareholders as dividends are taxed twice – once at the corporate level and again on the shareholder’s personal tax return.

Taxes: Salaries are subject to payroll taxes, while dividends are taxed at the capital gains rate.

Avoiding Common Mistakes

Distinguish Between Salaries and Dividends: Record dividends as distributions, not as an expense. Mixing the two can lead to incorrect financials and possible penalties.

Consider Tax Implications of Dividends: Since dividends are subject to double taxation, consult with a tax advisor for an optimal balance between salary and dividends.

Quick Reference Chart

How We Can Help

Properly recording owner’s compensation can be challenging, especially with different rules for each business type. While we’re not accountants or tax advisors, our expertise in QuickBooks ensures that your compensation transactions are accurately recorded and compliant with bookkeeping standards. At Veslav Consulting, we work with you to organize your QuickBooks accounts correctly, so your records are clean, clear, and ready for review by your tax professional. Contact us today to discuss how we can support your business bookkeeping needs!

Veslav Consulting

Simplifying Your Finances,

Empowering Your Growth

Contact Us

Join our newsletter list

858-308-1100

© 2025 Veslav Consulting. All rights reserved.