📞 (858) 308-1100

✉️ contact@veslav.com

Cash vs. Accrual Accounting Methods – Which is Right for Your Business?

11/1/20243 min read

When it comes to managing your business finances, choosing the right accounting method is one of the most important decisions you’ll make. The two primary accounting methods – cash and accrual – each provide distinct advantages and insights into your business’s financial health. In this post, we’ll explore the differences between these methods, how they impact your financial reports, and when each might be the best fit for your business.

What is the Cash Accounting Method?

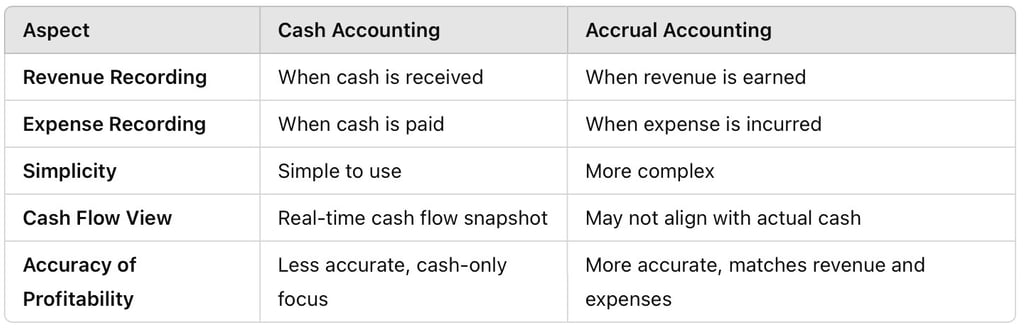

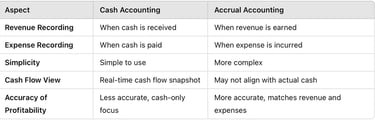

With cash accounting, you record income and expenses only when cash actually changes hands. Revenue is recognized when you receive payment, and expenses are recognized when you pay out money.

Example:

You send an invoice on May 1, but the customer pays you on June 15. With cash accounting, you record the income in June, when the payment was received.

Pros of Cash Accounting:

Simplicity: Cash accounting is straightforward and easy to implement, making it a good option for small businesses.

Real-Time Cash Flow View: Because transactions are recorded when cash is received or spent, you always have a clear picture of your cash position.

Cons of Cash Accounting:

Limited Insight into Financial Health: Since income and expenses are only recorded when cash moves, it doesn’t always reflect the full financial picture of your business.

Can Misrepresent Profitability: If you have outstanding invoices or unpaid bills, cash accounting may give a skewed view of your profitability.

What is the Accrual Accounting Method?

In accrual accounting, revenue and expenses are recorded when they are earned or incurred, regardless of when the cash is actually received or paid. This means you record income when you bill a customer and expenses when you receive a bill.

Example:

You send an invoice on May 1, and the customer pays on June 15. With accrual accounting, you record the income in May when the invoice is issued, not when it’s paid.

Pros of Accrual Accounting:

Comprehensive Financial View: Accrual accounting provides a full view of your income and expenses, even when cash hasn’t changed hands yet.

Better Matching of Income and Expenses: This method shows a more accurate picture of profitability by matching revenues with related expenses.

Cons of Accrual Accounting:

Complexity: Accrual accounting can be more complex, requiring a good understanding of revenue recognition and expense matching.

Cash Flow Tracking Challenges: Since income and expenses are recorded before cash changes hands, it can be harder to keep track of cash flow.

Key Differences Between Cash and Accrual Accounting:

When to Use Cash Accounting

Cash accounting is typically used by small businesses, sole proprietors, or service-based businesses that operate primarily on a cash basis. It’s especially useful if you don’t carry large inventory, your transactions are straightforward, and you prefer a simple approach to tracking cash flow. This method can also be more tax-friendly in certain cases, as you may only pay taxes on income you’ve actually received.

When to Use Accrual Accounting

Accrual accounting is required for companies with revenue over $25 million or those that keep inventory, but it’s also valuable for businesses of any size that want a comprehensive view of their financial performance. This method provides a clearer, more accurate picture of profitability by matching revenue with expenses incurred, making it ideal for companies with complex transactions, multiple income streams, or plans to grow. Accrual accounting is often recommended if you need to present financial reports to stakeholders, seek funding, or comply with Generally Accepted Accounting Principles (GAAP).

How to Choose the Right Method

If you’re just starting out and prefer simplicity, cash accounting may be an easier option to manage cash flow. However, if your business is growing, accrual accounting can offer valuable insights into performance that the cash method may overlook. It’s worth consulting with a financial advisor or accountant to help make the best decision for your business.

How We Can Help

Whether you use cash or accrual accounting, keeping your QuickBooks Online records accurate and well-organized is essential for reliable reporting. Our team specializes in setting up and maintaining both cash and accrual records in QuickBooks, so you can focus on running your business confidently. Contact us today to learn how we can support your bookkeeping, no matter which accounting method you choose!

Veslav Consulting

Simplifying Your Finances,

Empowering Your Growth

Contact Us

Join our newsletter list

858-308-1100

© 2025 Veslav Consulting. All rights reserved.